Driving Economic Growth with Financial Inclusion

.jpg?width=1000&height=525&name=_Tiburcio%20Sanz%20Railsbank%20Head%20of%20Fintech%20Solutions%20(2).jpg)

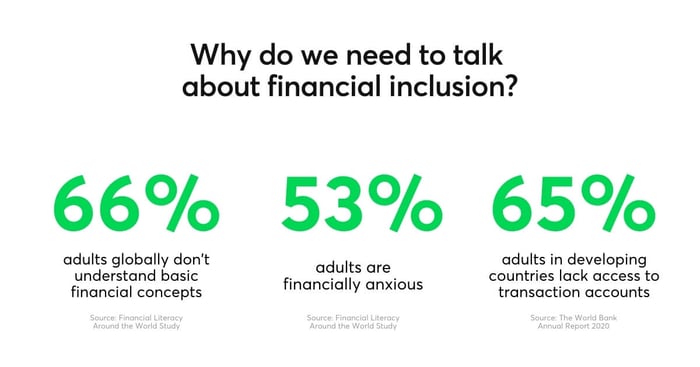

According to the World Bank Annual Report 2020, 65 percent of adults in developing countries still lack access to transaction accounts, let alone credit or insurance services that would help them plan for the future and improve standards of living. Despite the general agreement that digital financial services maximize economies of scale and increase the speed, security, and transparency of transactions, there is still not enough emphasis on financial inclusion – making these services widely available for all individuals.

High street banks still heavily rely on traditional data for identity verification, which excludes a big part of society from basic financial services. Even in mature economies, we have young people who might still live with their parents, which can mean that they don’t have credit scores or history as they look to start their adult lives.

On the other hand, access to internet and mobile devices is quickly growing, especially in emerging economies. “This is where fintech comes to play and can truly be a game changer,” says Tiburcio Sanz, Head of Fintech Solutions at Railsbank (Spain & Portugal), an open banking API and platform that gives regulated and unregulated companies access to global banking.

It is one of the companies that set out on a mission to “reinvent, unbundle, and democratize access to the complex, opaque, and byzantine 70-year-old credit card market, which is worth $4 trillion in the U.S. alone”, making the financial market inclusive.

I spoke with Tiburcio Sanz on the importance of financial inclusion, the challenges we face, and the steps that need to be taken to reinvent the current banking systems.

Why do we need to talk about financial inclusion?

Financial inclusion is a driver of development and a tool that helps people escape poverty. Together with financial education they are key components of a healthy and thriving society. They help prevent corruption, decrease admin costs, and improve efficiency of financial systems.

In fact, any kind of inclusion creates economic growth.

There is a big misconception that inclusion is a fancy treat we can only afford in times of prosperity. The economy is people and including more in more ways is what causes growth.

“If we look at recent research, 77% of us are stressed about money but hardly anyone talks about it. People who are constantly worried about financial security cannot be productive and focus on their jobs, families, and wellbeing,” Tiburcio says. “Even on Maslow’s pyramid of needs, we clearly see that without financial inclusion productivity and performance decreases,” he adds. It is a basic need that everyone should have equal access to.

The COVID-19 pandemic put an even bigger strain on home budgets. According to the latest edition of the ILO Monitor, an estimated 114 million people lost their jobs in 2020. Families who barely made ends meet before the pandemic were left alone without savings, fully dependent on help from the government or non-profit organizations. The lack of access to financial services deepens the wealth gap. Individuals unable to save, invest, and insure themselves against risks end up without opportunities to get out of poverty.

“Financial inclusion allows people to thrive both personally and professionally. Inequality, lack of opportunities, and debt burden tend to create a downward spiral that affects every echelon of our society,"

as Tiburcio sums up.

Inclusion starts with education

Tiburcio believes that financial education and changes in people’s relationship with money play a crucial role in making financial services inclusive to everyone. More conscious consumers can make informed decisions and plan with a long-term vision. “We currently live under constant bombardment of advertising that facilitates spending our money, or even money that we don’t have,” he says. “Without conscious spending and budgeting it is very easy to fall into debt and end up paying endless amounts of interest for things that we do not even use.”

Only a third of adults globally understand basic financial concepts. The vast majority don’t have the knowledge to manage finances - both their income and their expenditures - and to implement a plan for saving and investing. In result, they can easily fall into debt, mortgage defaults, or insolvency.

Many governments, aware of the importance of financial literacy, set out to implement frameworks that would help citizens obtain basic financial skills. Yet without enough funding or skilled professionals there is still a long way to go before personal finance courses are introduced to education systems, especially in emerging economies.

That’s why fintech companies have a chance to make a difference, at scale. As mentioned in the beginning, in a mobile-first reality people have more opportunities to obtain basic skills. Zogo is one of the apps that aims to improve financial knowledge. Based on the concept of "getting paid to learn," the app breaks down complicated financial topics into fun bite-sized modules. 97% of users reported Zogo has improved their financial literacy.

Innovation-driven financial inclusion

Innovation in the sector helps transform traditional institutions that are not designed for inclusion.

“With big data and AI, fintech companies are revolutionizing the market and helping end users budget, save and invest without even thinking about it.”

“Plum or Ikigai help users set up goals, vaults, roundups, cashbacks, and generate automated top-ups in their account without you even noticing,” Tiburcio adds.

These apps shift their focus from maximizing stakeholders’ interests to solving real human problems. They put people at the center of the strategy as they understand that’s what drives the economy and creates prosperity. Consumers with opportunities to build a stable financial future and grow wealth will have a chance to participate in the global economy. “By allowing end users to link their accounts and push payments directly to their platform of choice, we provide them with an easy and straightforward way of saving and investing their money,” Tiburcio sums up.

Fintechs open up opportunities on many fronts – from enabling easy digital payments, giving access to bank accounts without strict compliance checks, making purchases online in installments over a period of time (the popular buy now pay later business model), helping with savings, budgeting, and investing their capital. Thanks to technology, these products streamline the whole experience and solve the problem at its core.

By understanding the user, questioning assumptions, and redefining problems we can design products that empower users on many levels. Tiburcio gives an example that “if I ask the average person to try to put £200 aside per month, it is likely that by the end of the month those £200 would have already been spent. Now, if the app will automatically take £7 every other day, giving them reports on their spending and helping them to stay in line, they will see an instant improvement in their habits and as a consequence an increase in their savings.” But it won’t stop there.

“Once that person has saved a decent amount of money, the app can help them invest according to their risk appetite. Back in the day you had to be a savvy financial investor to be able to get into investing. Nowadays, and thanks to different fintechs that are shaping our financial lives, all the hassle is taken care of by them, in an easy, cost-effective way.”

Open banking boosts digital acceleration in fintech

Open banking platforms play a crucial role in driving the fintech (r)evolution. Platforms like Railsbank empower neobanks, retailers, and other entities to “develop the next generation of financial services that are embedded into customer journeys and centered around the consumer rather than around a legacy financial institution.”

Tiburcio Sanz points out that:

“All kinds of companies can embed financial services in their day-to-day operations and benefit from it.”

He adds: "Whether it’s an airline, a large retailer, a supermarket, or a car dealer, Railsbank can power their needs and help create their own ecosystem that will result in a faster, safer, and more economical setup than if they would try to build it themselves."

Open banking reduces costs and entry barriers for new service providers and increases go-to-market speed. Many more companies worldwide now have the chance to offer relevant products that address needs of the most underserved customers. This is another step towards financial inclusion and a simplified financial system that serves a wider spectrum of individuals.

“Open banking has allowed to level the playfield and increase iteration of payments. With the different platforms, we can only expect to see faster and cheaper ways of managing our money.

I truly believe that the next big change will involve B2B solutions and will enable merchants to build faster check out, cheaper ways of receiving money, and instant financing solutions for themselves, their suppliers, and their customers.”

Tiburico believes though that open banking is not a cure to financial exclusion and without education, consumer trust, and regulations provided by governments “it will only become an opportunity for a few instead of reaching every single stratum of society.”

There’s still a long way to go

We’re on a good path to make digital financial services accessible to consumers everywhere. However, there are many discrepancies when it comes to different markets, age groups, gender, or even race.

“The UK has been a natural leader in fintech and innovation, the EU is also doing great and we can see massive improvements in the USA and APAC. In these markets, many regulators want to support the natural evolution of these services. Just to give an example, during the London Fintech Week a UK government MP and a Cabinet Minister joined different panels and discussed how the landscape looks and what can be improved,” Tiburcio Sanz says.

While Western economies are leading the way, it tends to vary more in emerging markets. In Latin America we can see a clear division between different markets, as Tiburico points out. “Mexico, Brazil, and Colombia are taking enormous steps and embracing the fintech revolution. Others are lagging behind because the regulations impede flexibility and end up choking entrepreneurs who strive to innovate.”

Geography is not the only factor dividing the world when it comes to financial inclusion. In a recent interview with Asya Bradley, Founder & COO of First Boulevard, a neobank built for Black America, shared how racial discrimination and financial inequality are prominient in the Black communities in America. “People often think if you’re dealing with Black America, underbanked people, underserved people, they must be poor. That’s just not the case. Something I always want to emphasize is that building a product for underbanked people is not synonymous with saying we’re building a bank for poor people.”

Even though there is still a lot to be fixed on many levels, from government regulations to education, fintech companies are building the future of a cashless world where everyone can have access to basic financial services.

%20(1).jpg?width=362&height=241&name=tablet%20and%20flowers%20(1)%20(1).jpg)