Digital Innovation in Banking. “We Need to Change How We Used to Think of Life”

For instance, we will end up with people getting loans approved depending on the type and value of data they’re holding - says Anneli Bartholdy, Strategic Partner at Nordea.

She also believes that cryptocurrencies are here to stay and that banks need to stop seeing other banks as competition and start engaging in joint ventures.

Anneli Bartholdy works as a Strategic Partner at Nordea, Digital Innovation & Product Ownership Commercial and Business Banking. We sat down for a talk to explore:

- Which trends are to be followed by the banking industry in 2020?

- How are innovators in the banking industry undergoing digital transformation

- Why should banks change their model for evaluating risk and growth potential?

- What does she see as major blockers in the banking industry?

Let’s start with shedding more light on your role at Nordea.

My team is responsible for looking at what things will make starting or running a business easy or hard 2-3 years from now. We’re looking outside banking, thinking more broadly about our business customers’ ecosystems.

This is because we are trying to understand the dynamics of these changes and to design new products and services that can serve the future needs of entrepreneurs and businesses.

Are there any examples of these products that you could share?

We’re still working on the first potential concepts. But I can tell they all relate to how our customers can commercialise their data, how businesses can adjust to more sustainable business models and save money by doing less negative impact. Lastly, our concepts cover many things related to ecosystems and API-based activities.

So it's safe to say that your role as partner for digital innovation is neither forecasting the future tech nor designing new business models?

It’s definitely less about forecasting. We stay up to date but use the PESTLE framework to design scenarios instead of having one assumption about any given technology, which is what forecasting is in my opinion.

My focus is also not so much on business models. Our newly designed offerings may use existing or new business models, but at the end of the day, once we validate the solution, we apply what is relevant.

We assume that if we have a customer (can be existing or a new market of customers) buy-in validated, and a feasible solution, the rest is just practicalities to be sorted out.

What is your major challenge for 2020?

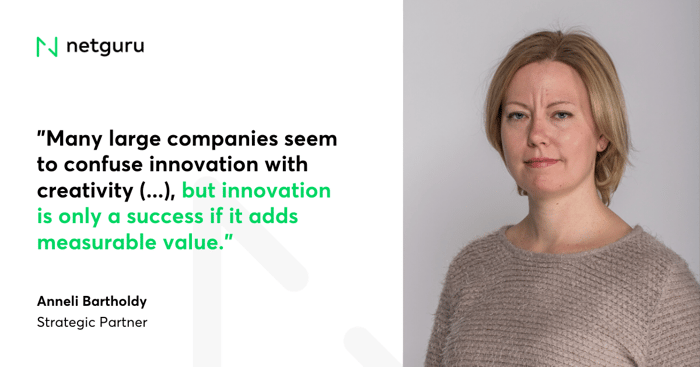

Realising value. Many large companies seem to confuse innovation with creativity in my opinion, but innovation is only a success if it adds measurable value, which may or may not be monetary. My challenge is to demonstrate that value in a very concrete and measurable way.

Speaking of innovation in the banking industry - what are the major blockers?

I think the industry is quite advanced compared to many others in Europe. However, the biggest blocker is seeing other banks as competition and not partners, especially within the same geographies. Our real competition is coming from elsewhere, so let’s stop pretending that we can protect ourselves by trying to out-invest each other by funding startups, and instead jointly develop or venture on new initiatives.

Which areas in banking or payments are most underserved?

I think there’s a bigger problem for banks - in most cases people and businesses are overserved. They’re spoiled for choice - they’ve got banks, fintechs targeting niche value propositions, and now tech giants with trusted names and familiar interfaces coming into the game. So really it's only a matter of time before banks are a commodity.

At the same time, banks are completely missing out on early funding for new businesses. When you’re running a SaaS or some other digital offering and have no assets to put up, but also don’t have money to fund early development, you’re too risky for a bank.

Do you believe that banks should embrace a less risk-averse model for investing?

In my opinion, banks use too much review of historical performance and guarantees, without sufficient understanding of how to evaluate risk and growth potential in emerging technologies and offerings. Banks also evaluate on an individual business request basis.

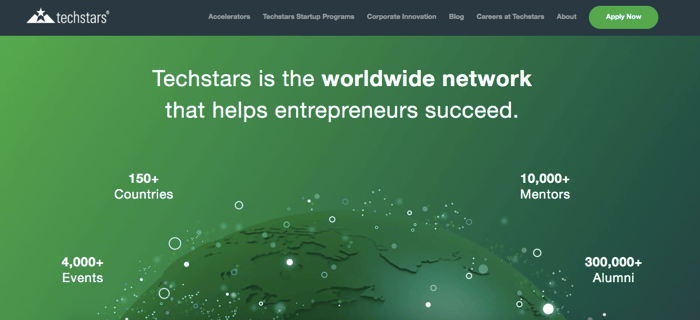

For instance, Techstars, a seed accelerator, gets payback in 1/200 investments, but at a sufficient level to balance the relatively small commitment into the other 199.

Banks risk evaluation methods are looking at one company and don’t know how to handle small requests, under 100,000 EUR. These are often seen more as personal loan requests since that’s a more relatable model for the bank to use, but it doesn’t recognize the business’s growth potential.

In the end, the banks and small businesses are both missing out by not accurately rating the risk of giving such small amounts measured against potential for business growth and success.

Innovation is a wide concept. What examples would you point out as a benchmark or inspiration for innovation in the banking industry?

There isn’t a benchmark in my opinion, because no one has gotten it completely right yet. The expanded definition of what a payment is and how it is done, for example with IoT, is very inspiring. I’m glad PDS2 came into effect and think we’ll see some creative new solutions coming out in the next couple of years.

The fact that customer data is shared between banks and licensed third parties also increases the pressure on banks to act more quickly to offer things that really make customers happy.

I believe, coming up, there will be a more dynamic and personalised way of understanding each individual customer based on data and insights. Instead of packages and lifecycle offerings designed for old-fashioned life plans and easy to manage at scale for banks, we’ll see more modular solutions that people can tailor to their needs.

What do you mean by “old-fashioned life plans”?

We used to think of a life as: grow up, study, get a partner, get a job, get a house, get kids, maybe change jobs once or twice within the same profession, educate your kids, retire, play with grandchildren, die.

Now a life could be: grow up, start a business, go to school, drop out, start a second business, meet a partner, save up for travel instead of home owning, become a consultant/freelancer, have a child, break up and remarry someone with two kids already, get a corporate job, get a new education, buy a house, move to Spain for 7 years, and Singapore for 2 years, quit at 55 to start your own business, work until you’re 70 with no owned property but with business assets and investments. Retire and freelance.

How people will be supported by financial institutions will be much better adapted to the unpredictable lifestyle and path people are more commonly being faced with today.

What is the single piece of advice you would give to a bank that is about to engage in a “digital transformation project”?

If you’re just starting, you’re too late. You now have two scenarios: first, to buy a much more advanced and mature company and product offering, and match your core to their setup and systems, instead of trying to integrate them into you.

Let go of ego and admit you’re the worse bet in the partnership and even if they’re smaller and younger. Let the other party set the pace, tone, way of working, and metrics.

The second scenario is that you can start trying to sell parts of your business off to the big techs and pick one or two niches you want to specialise in in the future. The niches should be hard to replicate and earn good money.

What trends will have a major impact on the banking industry in the next 3-5 years?

I believe we will get a new definition for value and for currency. Though banks don’t often seem to like cryptocurrencies, they are out there and won’t go away. I don’t see a difference between a group of people assigning value to a cryptocurrency and a group of people assigning value to a business. Both are subjective, risky, and in many cases not transparent.

What’s more, data will be quantified as an asset, more so than it is today. We will end up with people getting loans and financial benefits depending on the type of data they’re holding.

Which trend do you see as crucial for the banking industry to follow in 2020?

Green energy taking over as the standard. We aren’t using more solar and wind because we ran out of oil, we just needed green energy to be financially comparable to implement. Our bank solutions won’t stop being needed, but they may be offered in a better way for our customers by someone else. Sooner than we think. So we’re trying to get ready. But definitely the sustainable future is the one to watch, and to be part of.

Please note: All opinions expressed in the article are the individual’s and do not represent the opinions of Nordea.

You may also want to check Anneli Bartholdy’s insights on how digital transformation projects should be run and on strategies leaders should follow. Highly recommended read.