Own the change

We design, build, and scale all things digital for startups, scale-ups, and enterprises

Trusted by:

AI-driven digital acceleration

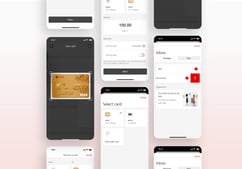

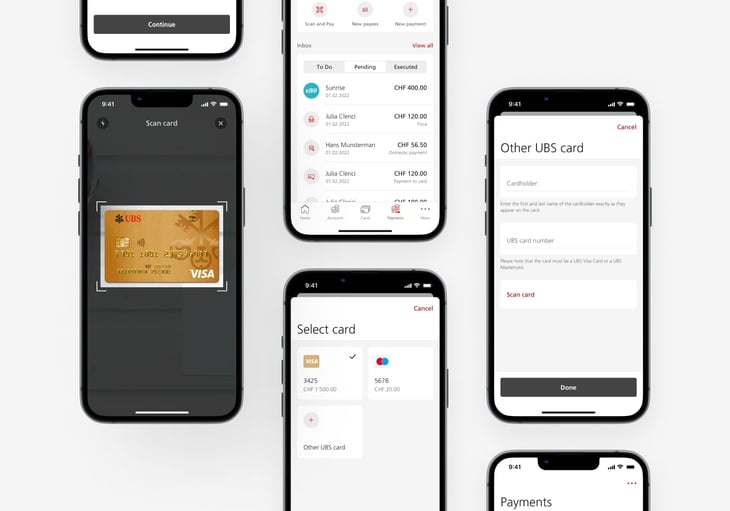

Mobile-first approach in the best-in-class banking app.

Seamless and consistent experience, unified payment flows, and easier in-app navigation

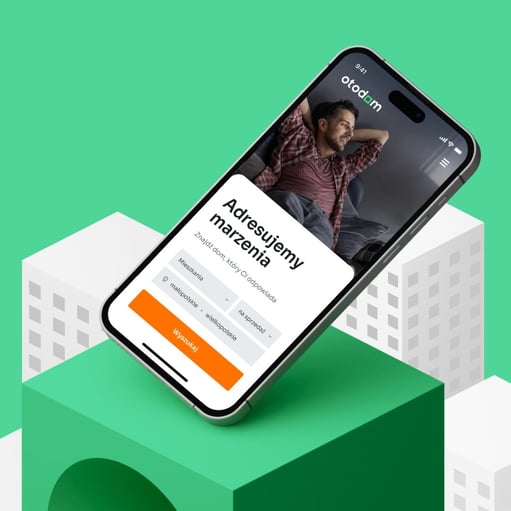

21% conversion increase with product design services for Otodom .

Augmenting highly demanding team with top-notch product design experts

97% faster inventory management with Flutter.

Real-time storage compliance monitoring thanks to a seamless cross-platform solution

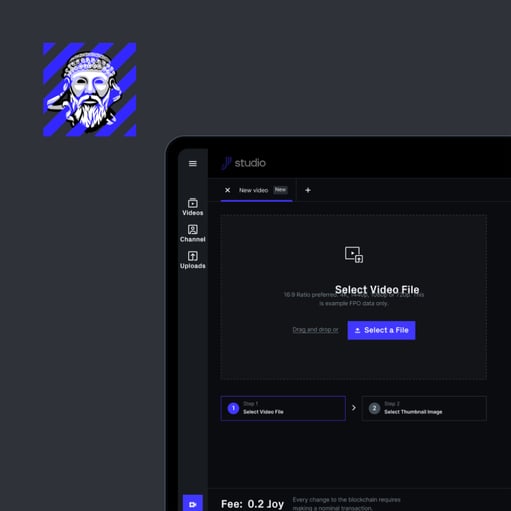

Exquisite look & feel for a blockchain video platform.

Top-notch viewing experience with research, design, and MVP development for an Oslo-based startup

Consistency across products with a design system.

Improved developer experience and more efficient engineering for the world's largest real estate franchise

Joyful customer experience with a virtual try-on.

Online sales boost with ML and augmented reality for a global cosmetics company

Full digital product expertise under one roof

Whether you want to consult an idea, add missing capabilities, quickly expand your team, or hand over a project – we’ve got you covered.

In our clients' words

Netguru always tries to make things possible.

Netguru has been the best agency we've worked with so far.

It doesn't feel like an external team, it feels like we're just working together.

Netguru has an incredible remote culture. It really makes working together easy.

With Netguru, we’re now releasing many more features than we used to.

Let me put it this way: we have built a grand and impressive building. But without Netguru’s insights, we would be stuck on the ground-floor forever.

Insights for change

Blog:

Generative AI Use Cases in Finance and Banking

Blog:

Enterprise AI-Powered Knowledge Base And Why We’ve Built One for Ourselves

Podcast:

Innovation Approach for the Corporates: How to Find One That Works

Blog:

10 Real-World Examples of How Team Extension Accelerates Delivery

Podcast:

Can Growth and Product Strategies Work Well Together? Disruption Talks with Hostelworld

.jpg?width=360&height=239&name=ux-indonesia-qC2n6RQU4Vw-unsplash%20(1).jpg)

Blog:

How AI Is Changing the Landscape of UX and Product Design

Tech as a force for good

Join us in initiatives that bring together problem solvers to tackle the big challenges of today.

Scaling up the fight to reduce carbon emissions with Coalition for Rainforest Nations

Helping an energy-tech startup increase clean energy access in sub-Saharan Africa

Relieving volunteers at a record-breaking annual charity fundraiser for pediatric care

Empowering a global community of women leaders with a scalable network hub

Build impactful products faster than the competition

Estimate project